Cheniere Energy LNG delivered an impressive fourth-quarter 2024 performance, beating both earnings and revenue estimates. The company reported adjusted earnings per share of $4.33, significantly surpassing the Zacks Consensus Estimate of $2.69. This outperformance was primarily driven by strong liquefied natural gas (“LNG”) shipments, with Cheniere loading 606 trillion British thermal units (TBtu) of LNG, exceeding the consensus mark of 582 TBtu.

Revenues for the quarter came in at $4.4 billion, slightly beating estimates by $31 million. However, this figure marked an 8% year-over-year decline due to moderating international gas prices. Despite this, Cheniere continues to exhibit strong financial health, maintaining its quarterly dividend of 50 cents per share and positioning itself as a key player in the LNG market.

Stock Performance and Consistent Earnings Surprises

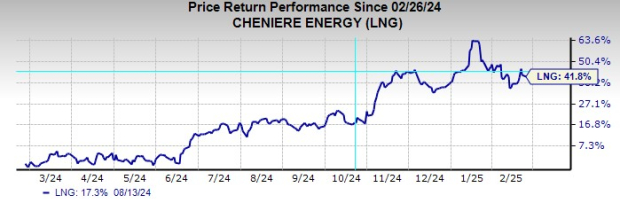

Cheniere’s stock has seen a remarkable 42% gain over the past year, reflecting investors’ confidence in the company’s long-term growth prospects.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

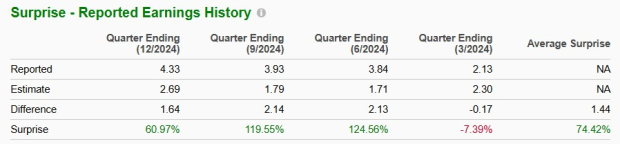

Additionally, Cheniere has consistently beaten the Zacks Consensus Estimate for earnings in three of the last four quarters, with an impressive trailing four-quarter earnings surprise average of 74.4%. This consistent outperformance highlights the company’s ability to navigate market challenges and capitalize on global LNG demand.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Strong Growth Drivers and Long-Term LNG Contracts

Cheniere’s success is underpinned by its long-term LNG supply agreements with major global energy players like Galp Energia GLPEY and Equinor EQNR. These contracts ensure stable revenue streams and provide protection against short-term price volatility in the LNG market. Furthermore, over the past 30 days, the Zacks Consensus Estimate for Cheniere’s 2025 EPS has moved up from $11.54 to $11.70, signaling growing optimism about the company’s future earnings potential.

The company is positioned to capitalize on the expected surge in global LNG demand, which is projected to nearly double by 2040, with 80% of growth driven by Asia. Cheniere Energy's strategic focus on expanding its liquefaction capacity at Sabine Pass and Corpus Christi, along with the high barriers to entry in the LNG export market, positions it as a leading supplier to meet this burgeoning demand, enhancing long-term revenue prospects.

Cheniere is also making strategic investments to expand its LNG infrastructure. The company’s Corpus Christi Liquefaction (CCL) Stage 3 project is progressing ahead of schedule, with the first LNG cargo produced in February 2025. Once fully operational, this expansion will boost Cheniere’s LNG production capacity by 20%, solidifying its position as the top U.S. LNG exporter.

Valuation Concerns: A Potential Headwind

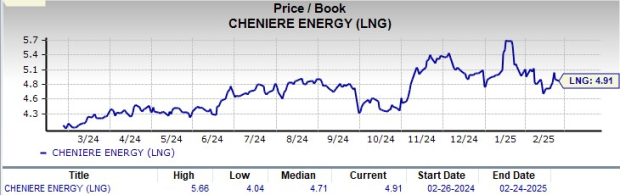

While Cheniere’s growth prospects remain strong, its valuation is a key concern. The stock currently trades at a price-to-book (P/B) ratio of 4.91, higher than its median of 4.71 and above many of its peers. This premium valuation may limit further upside potential, especially if LNG prices face downward pressure or global demand slows.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Another potential challenge is the rising cost of domestic natural gas, which could impact Cheniere’s margins. U.S. natural gas production has stagnated, and any sustained increase in input costs could reduce the company’s profitability. Additionally, trade conflicts and regulatory uncertainties could create headwinds for Cheniere’s expansion plans, particularly if geopolitical tensions shift LNG demand patterns.

Conclusion: Cheniere Stock Remains a “Buy”

Despite some valuation concerns, Cheniere Energy remains a compelling investment. Its strong Q4 performance, consistent earnings surprises, robust long-term contracts, and strategic LNG expansion efforts position the company for sustained growth. With impressive stock gain in the past year and upward earnings estimate revisions, Cheniere continues to be a dominant force in the LNG market. For investors seeking exposure to the growing LNG sector, Cheniere Energy appears well-positioned, making it a Zacks Rank #2 (Buy) at the current levels.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 256 positions with double- and triple-digit gains in 2024 alone.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cheniere Energy, Inc. (LNG): Free Stock Analysis Report

Galp Energia SGPS SA (GLPEY): Free Stock Analysis Report

Equinor ASA (EQNR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)