/Female%20scientist%20using%20microscope%20making%20lab%20analysis%20by%20aFotostock%20via%20Adobe%20Stock.jpeg)

Valued at a market cap of $27.5 billion, San Diego, California-based DexCom, Inc. (DXCM) is a medical device company that focuses on the design, development, and commercialization of continuous glucose monitoring (CGM) systems for the management of diabetes and metabolic health in the United States and internationally.

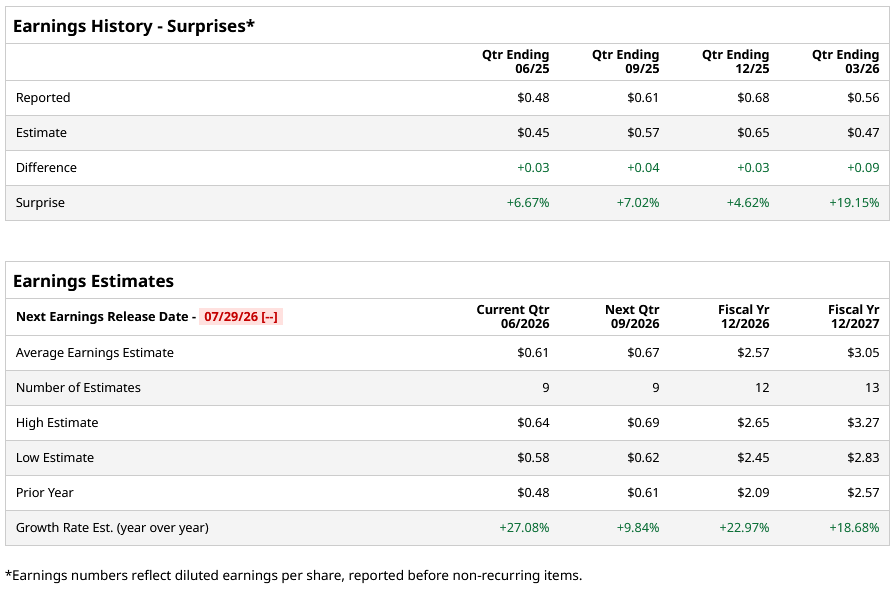

DXCM is expected to release its Q2 2026 earnings soon. Ahead of the event, analysts expect the company’s EPS to be $0.61 on a diluted basis, up 27.1% from $0.48 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in each of its last four quarters.

For fiscal 2026, analysts project the company’s EPS to be $2.57, up 23% from $2.09 in fiscal 2025. Moreover, its EPS is expected to rise by roughly 18.7% year over year (YoY) to $3.05 in fiscal 2027.

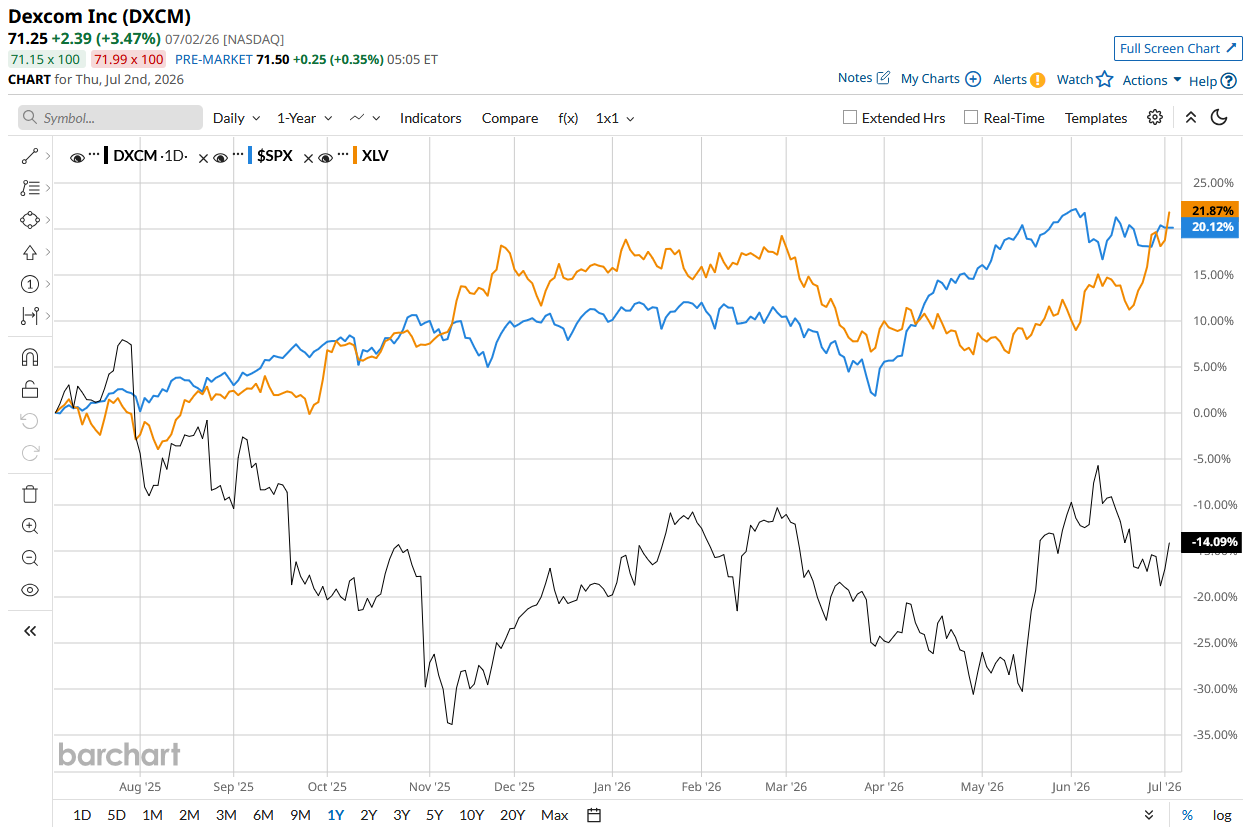

DXCM stock has declined 14.8% over the past 52 weeks, lagging behind the S&P 500 Index’s ($SPX) 19.2% rise and the State Street Healthcare Select Sector SPDR ETF’s (XLV) 21% rise during the same time frame.

On Apr. 30, DXCM stock rose 3.5% following the release of its Q1 2026 earnings. The company’s revenue for the quarter amounted to $1.2 billion and surpassed the Street’s estimates. Moreover, its adjusted EPS for the period came in at $0.56, also topping Wall Street’s forecasts. DexCom expects full-year revenue in the range of $5.16 billion to $5.25 billion.

Analysts are highly optimistic about DXCM, with the stock having a “Strong Buy” rating overall. Among the 28 analysts covering the stock, 23 are recommending a “Strong Buy,” one suggests a “Moderate Buy,” three recommend a “Hold,” and one suggests a “Strong Sell.” DXCM’s average analyst price target is $83.65, indicating an upside of 17.4% from the current levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)