/Semicondutors%20-%20closeup%20details%20of%20computer%20memory%20(RAM).jpg)

Lam Research Corporation (LRCX), headquartered in Fremont, California, designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits. Valued at $439.5 billion by market cap, the company’s products are used to deposit special films on a silicon wafer and etch away portions of various films to create a circuit design. The semiconductor giantis expected to announce its fiscal fourth-quarter earnings for 2026 in the near term.

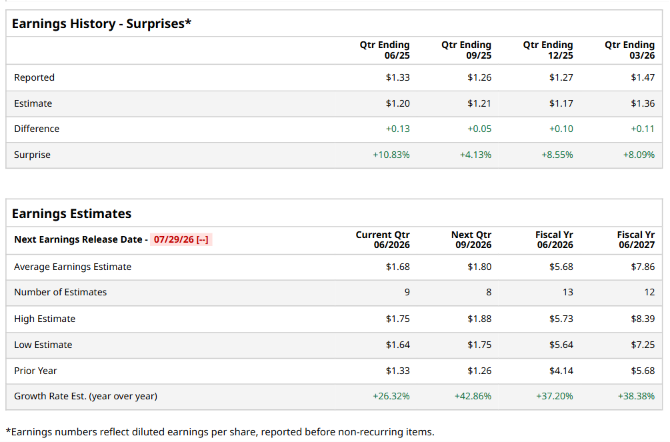

Ahead of the event, analysts expect LRCX to report a profit of $1.68 per share on a diluted basis, up 26.3% from $1.33 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect LRCX to report EPS of $5.68, up 37.2% from $4.14 in fiscal 2025. Its EPS is expected to rise 38.4% year over year to $7.86 in fiscal 2027.

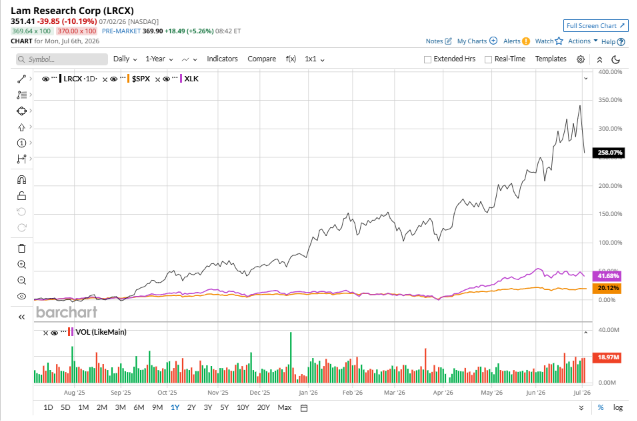

LRCX stock has significantly outperformed the S&P 500 Index’s ($SPX) 19.2% gains over the past 52 weeks, with shares up 255.6% during this period. Similarly, it considerably outperformed the State Street Technology Select Sector SPDR ETF’s (XLK) 42.4% gains over the same time frame.

LRCX’s outperformance is driven by AI-fueled demand for semiconductor manufacturing equipment. CEO Timothy Archer noted that the Customer Support Business Group hit a record $2 billion in quarterly revenue on growth in spares, upgrades, and services, while investments in advanced packaging, NAND, and DRAM for AI data centers boosted revenue and margins. Archer said “semiconductor technology inflections required for AI compute are driving higher deposition and etch intensity,” creating a multiyear growth setup. Guidance remains strong through 2027, supported by new memory and logic adoption, expanded operations including a Malaysia fab, and tools like Equipment Intelligence and Dextro cobots that improve customer productivity.

Analysts’ consensus opinion on LRCX stock is bullish, with a “Strong Buy” rating overall. Out of 33 analysts covering the stock, 22 advise a “Strong Buy” rating, four suggest a “Moderate Buy,” and seven give a “Hold.” LRCX’s average analyst price target is $360.91, indicating a potential upside of 2.7% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)