Wall Street analysts are turning cautious on Mastercard Incorporated MA stock, as evident from the southward estimate revisions and no upward movements. Over the past month, the Zacks Consensus Estimate for 2025 and 2026 EPS has dropped by 8 cents and a penny, respectively.

See the Zacks Earnings Calendar to stay ahead of market-making news.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

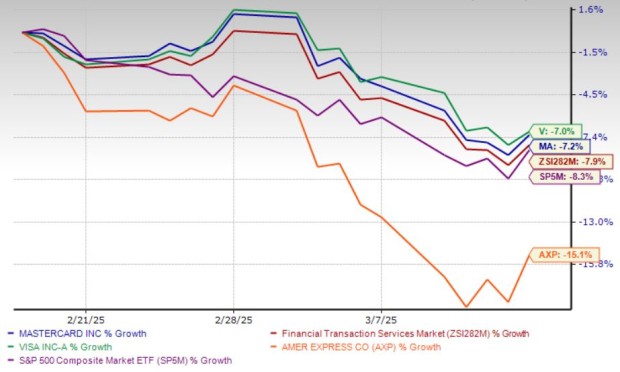

During the past month, shares of Mastercard have declined 7.2% compared with the industry’s and the S&P 500 Index’s declines of 7.9% and 8.3%, respectively. Meanwhile, peers like Visa Inc. V and American Express AXP were down 7% and 15.1%, respectively.

Price Performance – MA, V, AXP, Industry & S&P 500 Index

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Should you capitalize on Mastercard's recent dip? Let’s examine its operations, valuation and risks to make an informed decision.

Mastercard’s Operations Continue to Grow

MA’s gross dollar volume (GDV) increased 8.1% in 2024, following 10.3% growth in 2023. The Zacks Consensus Estimate for 2025 GDV indicates around 7% year-over-year growth. So, while the company is still expected to witness growth, the degree is expected to moderate.

Similarly, switched transactions increased 13.9% in 2023 and 11.3% in 2024. The consensus estimate for 2025 for the metric signals around a 10% year-over-year rise.

The company is investing heavily to meet the growing demand for its service offerings like cybersecurity and data analytics, facilitating its diversification efforts. In 2024, value-added services generated $10.8 billion, up 16.8% year over year, thanks to increasing demand for consumer acquisition, engagement, and business and market insights. Our model estimate suggests nearly 14% growth in 2025.

Mastercard's expansion in emerging markets, especially in Southeast Asia and Latin America, supports its long-term growth strategy. These efforts help offset revenue losses from its Russia exit while tapping into a vast, underbanked population. However, its massive international exposure could pose some risks due to geopolitical uncertainties.

The shift toward digital payments remains a major growth driver. As cash usage declines, Mastercard is leveraging its global network and expanding its service offerings to stay ahead. Its strong cash reserves enable organic growth and strategic acquisitions, ensuring continued expansion. Investments in AI, fraud prevention and digital solutions further solidify its leadership in the payments industry.

Mastercard’s Valuation is not Cheap

From a valuation perspective, Mastercard is trading at a forward P/E ratio of 32.08X, higher than its five-year median of 31.75X and well above the industry average of 22.78X. In comparison, Visa trades at 27.74X and American Express at 16.84X. Mastercard’s premium valuation raises overvaluation concerns.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Mastercard’s Risks

Along with growing operations, its expenses are also on the rise. Adjusted operating expenses have increased consistently, 10.7% in 2022, 10.5% in 2023 and 11% in 2024. Our model estimate indicates 13% growth in the metric in 2025. Meanwhile, rebates and incentives (a contra-revenue item) rose 16.1% year over year in 2024. We expect it to be around $18.8 billion in 2025, putting pressure on net revenue growth.

The company also faces legal and regulatory challenges. Last December, Mastercard settled a major London lawsuit related to card fees, while earlier this year, it resolved a pay bias lawsuit, agreeing to conduct pay audits and review its career advancement policies.

A key regulatory risk is the Credit Card Competition Act of 2023, aimed at reducing merchant fees and increasing competition in the payments industry. If passed, it could threaten Mastercard and Visa’s duopoly in the United States, potentially slowing revenue growth in a key market. The evolving political landscape in the payments industry could bring significant changes, with its full impact expected to unfold in the coming months.

Should You Buy Mastercard Stock Now?

Mastercard remains a long-term winner due to its strong global network, digital payment growth and AI-driven innovation. However, rising costs, regulatory challenges and an expensive valuation suggest limited near-term upside.

For existing shareholders, holding the stock makes sense. New investors, however, may want to wait for a better entry point. Mastercard currently has a Zacks Rank #3 (Hold), reflecting a neutral outlook. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/Quantum%20Computing/Image%20by%20Funtap%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Nike%2C%20Inc_%20shopping%20by-%20hapabapa%20via%20iStock.jpg)

/Quantum%20Computing/A%20concept%20image%20with%20a%20brain%20on%20top%20of%20a%20blue%20circuit%20board_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)