Palantir Technologies Inc. PLTR has experienced a 31% decline in its stock price over the past month, a drop largely attributed to the broader market downturn and increasing concerns over cost-cutting measures from the incoming administration. Losses spread across the sector. For instance, NVIDIA NVDA has gained 13%, International Business Machines IBM has climbed 6%, and Oracle ORCL has gained 17% in a month.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Being a volatile stock, this level of pullback is not entirely surprising. However, with PLTR’s strong fundamentals and robust growth prospects, it’s worth examining whether this dip presents a buying opportunity.

Palantir's Role in the Evolving AI Economy

We are in the midst of an AI boom characterized by rapid advancements and a proliferation of AI models. By 2026, the oversaturation of AI solutions is expected to become even more evident. Palantir has recognized this shift and strategically positioned itself to capitalize on the changing dynamics of the AI economy.

While many companies are engaged in an arms race to develop slightly improved AI models, Palantir differentiates itself by focusing on seamless AI integration into enterprise operations. The company refers to this approach as quantified exceptionalism, delivering transformative, measurable outcomes such as time savings, cost reductions and productivity enhancements.

At the core of Palantir’s strategy is its Artificial Intelligence Platform, which enables businesses to structure and organize their data — whether financial, supply chain, operational, or HR-related — so that AI can process and execute tasks more effectively. By leveraging an ontology-driven approach, Palantir creates digital representations of entire enterprises, allowing AI to interact seamlessly with business operations. Unlike companies that contribute to the oversupply of AI models, Palantir is actively shaping the demand side of the AI economy, positioning itself as a key player in enterprise AI adoption.

PLTR's Strong Financial Position and Growth Trajectory

Palantir’s financial health further reinforces its investment appeal. As of Dec. 31, 2024, the company held $5.2 billion in cash and equivalents, with zero debt, providing ample liquidity to invest in growth initiatives.

Moreover, Palantir’s recent financial performance underscores its strength. In 2024, revenues surged 29% year over year, with its U.S. commercial business experiencing 54% growth. The company has also secured several high-profile customer deals, including partnerships with Walgreens and Heineken, which have driven a bullish sentiment in the stock market. Additionally, Palantir has formed strategic alliances with TWG Global, EYSA, Voyager and Databricks, further solidifying its market position.

Upbeat Earnings Projections and Analyst Confidence

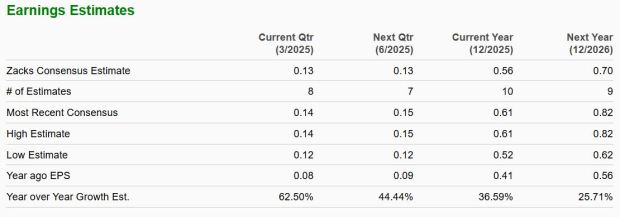

The Zacks Consensus Estimate for Palantir’s first-quarter 2025 earnings stands at 13 cents per share, reflecting 62.5% year-over-year growth. For 2025 and 2026, earnings are projected to rise 37% and 26%, respectively, compared to prior-year figures. Sales are also expected to see robust growth, increasing 36.3% in the first quarter of 2025, with full-year sales projected to rise 32.2% in 2024 and 27.9% in 2025.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Analyst sentiment further reinforces this positive outlook. Over the past 60 days, six upward earnings estimate revisions have been recorded for the first quarter of 2025, with no downward adjustments. Similarly, nine upward revisions for 2025 and five for 2026 highlight growing confidence in Palantir’s trajectory. The Zacks Consensus Estimate for 2025 earnings has increased by 16.7%, while the 2026 estimate has risen by 20.7%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Yes! A Buy-the-Dip Opportunity

Palantir’s significant stock decline may appear concerning, but its strong financials, impressive growth trajectory, and strategic positioning in the AI economy suggest a compelling investment case. The company is capitalizing on the evolving AI landscape, focusing on enterprise integration rather than just AI model development. With a debt-free balance sheet, expanding customer base, and analyst optimism, PLTR appears well-positioned for long-term growth.

Given these factors, investors may view this pullback as a buy-the-dip opportunity, especially as Palantir continues to execute its strategy and generate real, quantifiable value for its clients and shareholders.

PLTR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

International Business Machines Corporation (IBM): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/Technology%20abstract%20by%20Joshua%20Sortino%20via%20Unsplash.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)