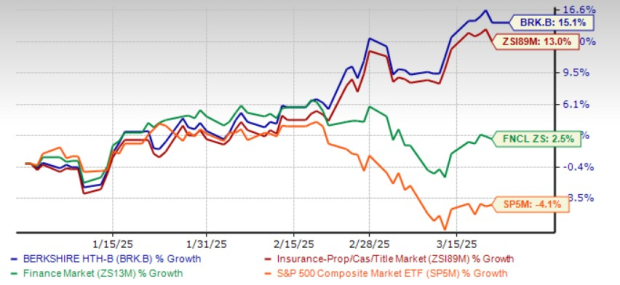

Shares of Berkshire Hathaway Inc. (BRK.B) have gained 15.1% year to date, outperforming the industry’s 13% growth, the Finance sector’s rise of 2.5% and the S&P 500 composite’s decline of 4.1%.

BRK.B shares are trading near the high end of its 52-week range of $530.61.Berkshire Hathaway shares are trading well above the 50-day moving average, indicating a bullish trend.

With a market capitalization of more than $1.1 trillion, Berkshire Hathaway is a conglomerate with more than 90 subsidiaries engaged in diverse business activities. BRK.B’s property and casualty insurance business, one of the largest property and casualty insurance companies, generates the maximum return on equity.

Berkshire Hathaway Outperforms Industry, Sector & S&P YTD

Image Source: Zacks Investment Research

Average Target Price for BRK.B Suggests Downside

Based on short-term price targets offered by four analysts, the Zacks average price target is $504.75 per share. The average suggests a potential 3.3% downside from the last closing price.

Image Source: Zacks Investment Research

What’s Working in Favor of Berkshire Hathaway?

Among its diverse business activities, its insurance operations are the most important, accounting for about one-fourth of BRK.B’s top line. The insurance business is poised for long-term growth, banking on increased exposure, prudent underwriting standards and better pricing.

Continued insurance business growth fuels an increase in float, drives earnings and generates maximum return on equity.

Utilities and Energy (the other two largest businesses outside of insurance), Manufacturing, Service and Retail — Berkshire Hathaway’s economically sensitive non-insurance businesses — are performing well. The Utilities and Energy business has grown with increased revenue contributions from Burlington Northern SantaFe Corp. However, unfavorable changes in the business mix and lower fuel surcharge revenues are areas of concern. Demand for utilities is expected to be strong in the future and drive earnings growth.

Increasing demand for goods and services, given an improved economic backdrop, should benefit its Manufacturing, Service and Retail operations.

Collectively, these have driven revenues and facilitated margin expansion over the past many years.

With a huge cash hoard, BRK.B’s inorganic growth story remains impressive. The company eyes acquisitions of entities that have steady earning power and generate impressive returns on equity. While big acquisitions open up more business opportunities for the company, bolt-on acquisitions enhance earnings of the existing business.

Warren Buffett has always eyed acquisitions or made investments in properties that are undervalued or have potential for growth. The insurer has also started increasing its investment in Japan.

Berkshire Hathaway's liquidity helps it repurchase shares regularly, which is an effective capital deployment to distribute wealth to shareholders.

BRK.B Shares Seem Expensive

The stock is overvalued compared with its industry. It is currently trading at a price-to-book multiple of 1.73, higher than the industry average of 1.63. However, we believe that given BRK.B's dominant market presence, diverse business activities, and, above all, the name Warren Buffet, a premium valuation is quite justified for this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

It is attractively valued compared with other insurers like The Progressive Corporation PGR and The Allstate Corporation ALL.

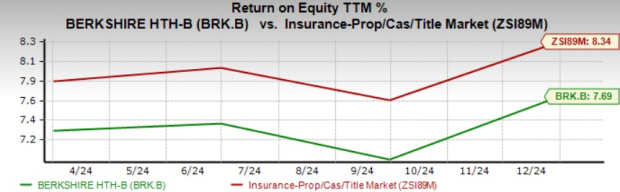

Berkshire Hathaway’s Return on Capital

Return on equity in the trailing 12 months was 7.7%, underperforming the industry average of 8.3%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders. It is noteworthy that though BRK.B’s ROE is lagging the industry average, the company has been continuously generating improved ROE.

Image Source: Zacks Investment Research

The same stays true for return on invested capital (ROIC), which has increased every year since 2020. This reflects BRK.B’s efficiency in utilizing funds to generate income. However, ROIC in the trailing 12 months was 6.1%, lower than the industry average of 6.4%.

Image Source: Zacks Investment Research

Mixed Analyst Sentiment

The Zacks Consensus Estimate for 2025 implies an 8% year-over-year decrease, while the same for 2025 suggests an 8.3% increase.

The consensus estimate for 2025 and 2026 moved 0.5% and 0.2% south in the last seven days, respectively.

Image Source: Zacks Investment Research

What to do With BRK.B Shares?

Warren Buffet stated that though more than 100 of 189 operating businesses reported a decline in earnings in 2024, Berkshire Hathaway fared better than Buffet’s expectation. That was primarily due to a large gain in investment income as Treasury Bill yields improved and the company increased holdings of these highly liquid short-term securities. That is Berkshire Hathaway for you. Holding shares of the company renders dynamism to one’s portfolio.

Also, BRK.B has Warren Buffett at its helm, who has been creating tremendous value for shareholders over nearly six decades with his unique skills.

Thus, investors who already hold Berkshire Hathaway shares should continue to retain them in their portfolios. However, given its premium valuation, new investors can wait for a better entry point.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.3% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Berkshire Hathaway Inc. (BRK.B): Free Stock Analysis Report

The Allstate Corporation (ALL): Free Stock Analysis Report

The Progressive Corporation (PGR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

/Quantum%20Computing/Image%20by%20Funtap%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Nike%2C%20Inc_%20shopping%20by-%20hapabapa%20via%20iStock.jpg)

/Quantum%20Computing/A%20concept%20image%20with%20a%20brain%20on%20top%20of%20a%20blue%20circuit%20board_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)